Introduction

PPO vs HMO health plans is one of the most important comparisons consumers make when selecting health insurance. Are you wondering which plan offers better flexibility, lower costs, or access to your preferred doctors? Choosing the wrong health plan can lead to higher medical expenses and limited healthcare options. Understanding the differences between PPO and HMO plans helps individuals and families select coverage that fits their healthcare needs and financial goals. By comparing provider networks, referral requirements, premiums, deductibles, and overall benefits, consumers can confidently choose the right insurance plan while protecting both their health and long-term financial security.

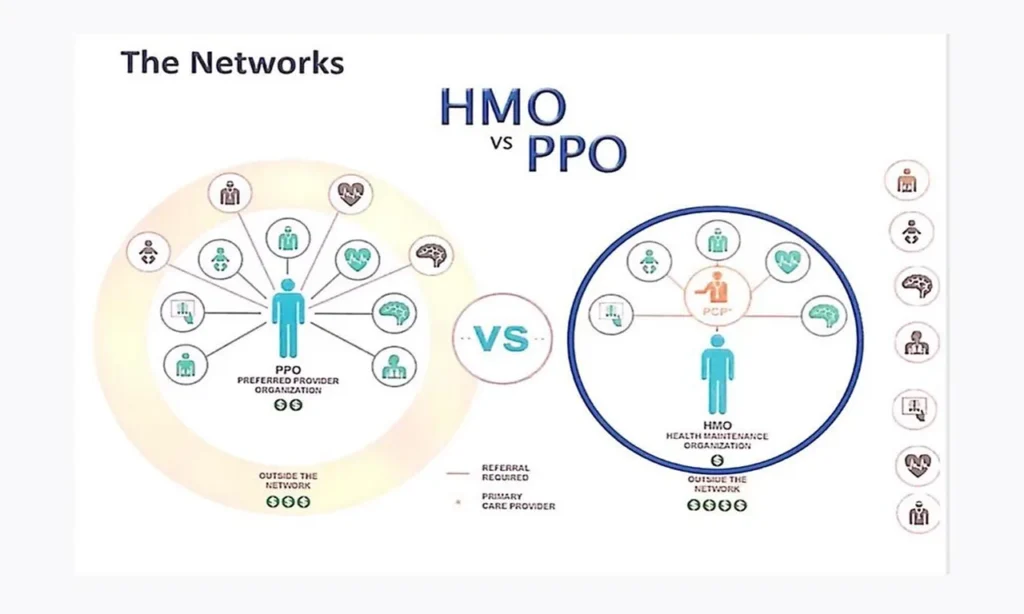

Understanding PPO Vs HMO Health Plans Differences Clearly

PPO vs HMO health plans differ primarily in provider flexibility, referral requirements, and overall healthcare costs. PPO plans generally allow members to visit specialists without referrals and receive partial coverage outside the provider network. HMO plans require members to select a primary care physician and obtain referrals before seeing specialists. Although HMOs often have lower premiums, PPOs provide greater healthcare freedom. Understanding these core differences helps consumers compare both plan types carefully and select the option that best matches their medical needs and financial priorities.

Why PPO Vs HMO Health Plans Matter Today

Healthcare costs continue rising, making PPO vs HMO health plans an important decision for individuals seeking affordable medical coverage. The right insurance plan influences healthcare accessibility, provider choices, specialist visits, and long-term medical expenses. Consumers who understand plan differences avoid unnecessary costs while maximizing healthcare benefits. Comparing both options carefully ensures better financial planning and more appropriate healthcare coverage. Selecting the right health insurance supports long-term wellness while protecting families from unexpected medical expenses and complicated insurance decisions.

How PPO Health Insurance Plans Actually Work Today

Within the PPO vs HMO health plans comparison, PPO plans provide members with greater flexibility when choosing healthcare providers. Individuals may visit specialists without referrals and receive partial coverage even when using out-of-network physicians. PPO policies typically maintain larger provider networks, allowing greater healthcare freedom. However, these benefits often result in higher monthly premiums and deductibles. Understanding PPO plan structures helps consumers determine whether expanded provider access justifies additional healthcare expenses and insurance costs.

How HMO Health Insurance Plans Function Efficiently

When comparing PPO vs HMO health plans, HMO policies focus on coordinated healthcare through primary care physicians. Members choose one primary doctor who manages routine care and provides referrals for specialist treatment. Healthcare services usually remain limited to participating providers within the network except during emergencies. HMOs often feature lower premiums, reduced out-of-pocket expenses, and predictable healthcare costs. Understanding HMO operations helps consumers determine whether coordinated care and lower costs meet their healthcare preferences and financial objectives.

Comparing Provider Networks Between PPO And HMO Plans

One major difference in PPO vs HMO health plans involves provider network flexibility. PPO plans generally offer larger provider networks and partial reimbursement for out-of-network medical services. HMO plans usually require members to receive treatment from participating healthcare providers except during emergencies. Individuals with preferred physicians should verify network participation before enrolling. Understanding provider network differences allows consumers to maintain continuity of care while selecting insurance plans that best support healthcare accessibility and long-term medical relationships.

Referral Requirements Under PPO Vs HMO Health Plans

Referral policies remain a key distinction between PPO vs HMO health plans. PPO members usually schedule appointments directly with specialists without primary care referrals. HMO members typically need authorization from their primary physician before receiving specialist treatment. Although referral systems encourage coordinated healthcare management, they may delay access to specialized services. Consumers should evaluate personal healthcare needs before choosing between unrestricted specialist access and coordinated medical care. Understanding referral requirements improves healthcare planning and overall insurance satisfaction.

Monthly Premium Costs Comparing PPO And HMO Plans

Premium differences significantly influence PPO vs HMO health plans purchasing decisions. PPO plans generally require higher monthly premiums because they offer greater provider flexibility and broader healthcare access. HMO plans usually provide lower monthly costs while restricting provider choices to network participants. Consumers should compare premiums alongside deductibles, copayments, and expected medical usage before selecting coverage. Understanding premium structures helps individuals balance affordability with healthcare flexibility while supporting responsible long-term financial planning.

Deductibles And Out Of Pocket Expenses Compared Carefully

When evaluating PPO vs HMO health plans, consumers should compare deductibles, copayments, coinsurance, and annual out-of-pocket maximums instead of focusing only on premiums. PPO plans often include higher deductibles and greater personal healthcare expenses before insurance coverage increases. HMO plans generally offer lower deductibles and reduced out-of-pocket costs for in-network care. Understanding total healthcare expenses provides a clearer picture of long-term insurance value. Careful cost comparisons support better financial planning and smarter healthcare decisions.

Specialist Access Under PPO Vs HMO Health Plans

Specialist access remains one of the biggest considerations within PPO vs HMO health plans. PPO members usually contact specialists directly without referral requirements, allowing faster access to specialized medical care. HMO members generally receive specialist services after obtaining referrals from primary care physicians. Individuals requiring frequent specialist treatment often value PPO flexibility despite higher costs. Understanding specialist access differences helps consumers select insurance plans supporting ongoing medical needs while balancing convenience with healthcare affordability.

Emergency Healthcare Coverage Across Both Insurance Plans

Emergency medical treatment remains covered under both PPO vs HMO health plans, although policy details may differ regarding non-emergency follow-up care and provider reimbursement. Emergency services generally receive coverage regardless of provider network status. After emergency stabilization, HMO members may need network providers for continued treatment, while PPO members often maintain greater provider flexibility. Understanding emergency healthcare provisions ensures consumers remain financially protected during unexpected medical crises while selecting appropriate insurance coverage.

Prescription Drug Benefits Comparing PPO And HMO Coverage

Prescription medication benefits should be reviewed carefully when comparing PPO vs HMO health plans. Although both plan types usually include prescription drug coverage, formularies, pharmacy networks, copayments, and medication tiers often vary. Individuals requiring ongoing medications should compare pharmaceutical benefits before enrolling. Understanding prescription coverage helps consumers estimate future healthcare expenses accurately while ensuring continued access to necessary medications. Careful comparison improves overall insurance value and long-term healthcare affordability.

Preventive Healthcare Services Included Within Both Plans

Preventive healthcare remains an important benefit offered under both PPO vs HMO health plans. Annual physical examinations, vaccinations, wellness visits, health screenings, and preventive diagnostic services help identify medical conditions before they become serious. Most preventive services receive coverage when using participating providers according to plan requirements. Understanding preventive healthcare benefits encourages regular medical checkups while reducing future treatment expenses. Preventive care supports healthier lifestyles and strengthens long-term financial protection against major medical conditions.

Families Choosing Between PPO And HMO Insurance Plans

Families often compare PPO vs HMO health plans to balance healthcare quality, provider flexibility, and monthly insurance costs. Parents should evaluate pediatric care, specialist availability, preventive services, emergency coverage, and prescription benefits before selecting family insurance. HMO plans frequently offer lower family premiums, while PPO plans provide greater physician choice. Understanding family healthcare priorities helps households select insurance matching both medical requirements and financial budgets while ensuring dependable healthcare access for every family member.

Self Employed Individuals Comparing PPO HMO Coverage Options

Self-employed professionals frequently evaluate PPO vs HMO health plans because they purchase healthcare independently without employer-sponsored coverage. Entrepreneurs, freelancers, consultants, and contractors should compare premiums, provider networks, deductibles, prescription coverage, and specialist access carefully. Healthcare flexibility may benefit business owners who travel frequently or require specialized medical services. Understanding insurance differences helps self-employed individuals choose affordable healthcare protection while maintaining continuous medical coverage and supporting long-term financial security.

Common Mistakes Choosing PPO Or HMO Health Plans

Many consumers comparing PPO vs HMO health plans focus only on monthly premiums while overlooking provider networks, referral requirements, deductibles, prescription benefits, and total healthcare expenses. Selecting coverage without evaluating expected medical needs may result in unnecessary costs or limited provider access. Comparing complete policy details rather than premium prices alone leads to smarter healthcare decisions. Understanding these common mistakes helps individuals maximize insurance value while securing reliable long-term healthcare protection.

Understanding Out Of Network Healthcare Coverage Benefits Clearly

One of the biggest differences in PPO vs HMO health plans involves out-of-network coverage. PPO plans usually provide partial reimbursement when members receive care from non-participating healthcare providers, although personal costs remain higher. HMO plans generally require members to stay within approved provider networks except during emergencies. Consumers who frequently travel or already have preferred physicians outside local networks often value PPO flexibility. Understanding out-of-network coverage helps individuals choose insurance that matches their healthcare preferences while avoiding unexpected medical expenses.

Choosing Primary Care Physicians Under Both Insurance Plans

Primary care physicians play different roles in PPO vs HMO health plans. HMO members must select a primary physician who coordinates healthcare services and manages specialist referrals. PPO members may choose primary physicians without mandatory referral requirements, allowing greater flexibility. Consumers who appreciate coordinated healthcare often prefer HMOs, while individuals seeking independent medical decisions may favor PPOs. Understanding primary care responsibilities helps buyers select insurance plans that align with personal healthcare management preferences and long-term medical needs.

Comparing Healthcare Costs Beyond Monthly Insurance Premiums Today

Evaluating PPO vs HMO health plans requires comparing total healthcare expenses rather than monthly premiums alone. Deductibles, copayments, coinsurance, prescription costs, specialist visits, and annual out-of-pocket maximums all influence overall affordability. PPO plans generally involve higher long-term costs but provide greater provider flexibility. HMO plans typically reduce healthcare expenses through coordinated network care. Understanding complete healthcare costs helps consumers make financially responsible insurance decisions while maximizing healthcare value throughout the policy year.

Prescription Medication Networks Between PPO And HMO Plans

Prescription drug coverage remains an important comparison within PPO vs HMO health plans. Although both plan types usually provide pharmacy benefits, participating pharmacy networks, medication formularies, and copayment structures often differ. Consumers requiring ongoing prescriptions should verify medication coverage before enrollment. Comparing pharmacy networks helps individuals avoid unnecessary prescription expenses while ensuring continued access to required medications. Strong pharmaceutical benefits improve healthcare affordability and overall satisfaction with selected insurance coverage.

Healthcare Flexibility Offered By PPO Insurance Coverage Plans

Flexibility remains one of the greatest advantages within PPO vs HMO health plans. PPO members enjoy greater freedom when selecting physicians, specialists, hospitals, and medical facilities. Referral requirements rarely limit healthcare decisions, allowing faster access to specialized treatment. Although flexibility generally increases insurance costs, many consumers value the convenience and independence provided by PPO plans. Understanding healthcare flexibility helps buyers determine whether expanded provider choice justifies higher premiums and overall medical expenses.

Lower Healthcare Costs Associated With HMO Insurance Plans

Cost savings represent one of the strongest benefits of PPO vs HMO health plans when evaluating HMO coverage. Lower premiums, reduced deductibles, and predictable copayments often make HMOs attractive for budget-conscious consumers. Coordinated healthcare management also helps control unnecessary medical spending through primary care oversight. Individuals who primarily use in-network providers frequently benefit from significant long-term savings. Understanding HMO cost advantages helps consumers balance healthcare affordability with quality medical services and dependable insurance protection.

Comparing Preventive Healthcare Services Across Both Plans Carefully

Preventive care remains a valuable benefit included within PPO vs HMO health plans. Annual wellness examinations, vaccinations, preventive screenings, physicals, and health assessments help identify medical conditions before expensive treatments become necessary. Both PPO and HMO plans generally cover preventive services when policy requirements are met. Regular preventive care improves long-term health outcomes while reducing future healthcare expenses. Understanding preventive coverage encourages consumers to utilize available wellness benefits and maintain healthier lifestyles throughout their insurance coverage.

Travel Considerations When Selecting PPO Or HMO Coverage

Frequent travelers should carefully evaluate PPO vs HMO health plans before choosing medical insurance. PPO plans often provide broader nationwide provider access and partial reimbursement for out-of-network treatment, making them attractive for business travelers and individuals who relocate frequently. HMO plans generally emphasize local provider networks except during emergencies. Understanding travel-related healthcare benefits helps consumers maintain continuous medical access regardless of location while minimizing unexpected treatment expenses away from home.

Young Professionals Comparing PPO And HMO Insurance Benefits

Young adults entering the workforce often compare PPO vs HMO health plans when selecting their first independent health insurance policy. Individuals with limited healthcare needs may appreciate HMO affordability, while professionals preferring provider flexibility often choose PPO plans. Comparing premiums, preventive care, specialist access, and emergency coverage helps younger consumers make informed insurance decisions. Understanding available healthcare options establishes a strong financial foundation while ensuring reliable medical protection during early career development.

Retirees Evaluating PPO Vs HMO Health Plans Carefully

Retirees frequently analyze PPO vs HMO health plans because ongoing healthcare needs often increase with age. Access to specialists, prescription medications, preventive services, and chronic disease management becomes increasingly important. PPO plans provide greater provider flexibility, while HMO plans emphasize coordinated care and lower healthcare expenses. Understanding retirement healthcare priorities helps older adults select insurance supporting both medical needs and financial stability. Appropriate coverage contributes to healthier aging and improved long-term healthcare experiences.

Employer Sponsored PPO And HMO Insurance Comparisons Explained

Many employers offer both PPO vs HMO health plans during annual benefits enrollment. Employees should compare premiums, deductibles, provider networks, specialist access, prescription coverage, and employer premium contributions before selecting coverage. Employer-sponsored plans may significantly reduce healthcare costs through shared premium payments. Understanding available workplace insurance options helps employees maximize healthcare benefits while making financially responsible enrollment decisions. Careful comparison supports stronger medical protection and long-term employee satisfaction.

Specialist Healthcare Access Without Referral Requirements Explained

One important feature of PPO vs HMO health plans is direct specialist access available through PPO coverage. Members usually schedule appointments independently without obtaining primary care referrals, reducing delays for specialized treatment. HMO plans generally require referral approval before specialist visits. Individuals managing chronic illnesses or requiring frequent specialist care often appreciate PPO convenience despite higher premiums. Understanding specialist access differences improves insurance selection while supporting timely medical treatment and comprehensive healthcare management.

Understanding Claims Process Under PPO Insurance Plans Clearly

Claims procedures differ slightly within PPO vs HMO health plans, particularly when using out-of-network healthcare providers. PPO members occasionally submit reimbursement claims after receiving treatment outside participating networks. In-network services usually process automatically through healthcare providers. Understanding PPO claims procedures helps consumers avoid administrative delays while maximizing insurance benefits. Familiarity with documentation requirements also improves reimbursement efficiency and overall satisfaction throughout healthcare experiences.

Healthcare Coordination Advantages Offered By HMO Insurance Plans

Coordinated healthcare represents one of the greatest strengths within PPO vs HMO health plans when evaluating HMO coverage. Primary care physicians oversee patient treatment, coordinate specialist referrals, monitor preventive services, and maintain complete medical histories. This structured approach often improves continuity of care while reducing duplicate testing and unnecessary healthcare expenses. Understanding coordinated healthcare benefits helps consumers appreciate the long-term value offered by HMO insurance despite reduced provider flexibility.

Annual Healthcare Reviews Improve Insurance Plan Selection Decisions

Regularly reviewing PPO vs HMO health plans ensures healthcare coverage continues matching changing medical needs and financial priorities. Healthcare usage, family size, employment status, and preferred physicians may change over time. Annual policy comparisons allow consumers to identify stronger benefits, improved provider networks, or lower overall costs. Reviewing insurance options during Open Enrollment supports informed healthcare decisions while maintaining comprehensive medical protection throughout changing life circumstances.

Technology Improving PPO And HMO Insurance Services Rapidly

Digital innovation continues enhancing PPO vs HMO health plans through mobile applications, telemedicine services, online provider directories, electronic claims processing, and secure customer portals. Consumers can compare benefits, schedule appointments, monitor claims, and access insurance documents electronically. Technology improves convenience while reducing administrative complexity. Understanding available digital healthcare tools helps policyholders maximize insurance efficiency and receive faster support throughout their healthcare experiences.

Future Healthcare Trends Affecting PPO HMO Insurance Markets

The healthcare industry continues transforming PPO vs HMO health plans through artificial intelligence, digital healthcare platforms, wearable technology, personalized medicine, and expanded telehealth services. Insurance companies increasingly adopt innovative technologies to improve affordability and patient experiences. Consumers who understand future healthcare developments can better prepare for evolving insurance options. Staying informed supports smarter healthcare planning while maximizing long-term insurance value and medical protection.

Financial Planning Using PPO And HMO Health Coverage

Effective financial planning requires understanding PPO vs HMO health plans beyond monthly premium comparisons. Consumers should evaluate annual medical expenses, deductibles, specialist visits, prescription costs, and healthcare utilization before selecting insurance. Proper planning helps households balance healthcare affordability with comprehensive medical protection. Understanding total healthcare spending encourages smarter insurance decisions while protecting long-term financial stability and reducing unexpected medical expenses.

Avoiding Common PPO And HMO Insurance Selection Mistakes

Many consumers comparing PPO vs HMO health plans focus exclusively on premiums while ignoring provider flexibility, referral requirements, prescription benefits, and expected healthcare usage. Choosing insurance without considering future medical needs often results in dissatisfaction and unnecessary expenses. Comparing complete policy features improves healthcare planning while maximizing insurance value. Understanding common purchasing mistakes helps consumers make informed decisions and secure dependable long-term medical coverage.

Choosing PPO Vs HMO Health Plans Confidently Today

Selecting between PPO vs HMO health plans requires careful evaluation of healthcare flexibility, provider networks, premiums, deductibles, referral policies, prescription coverage, and expected medical needs. Consumers who compare both options thoroughly often achieve stronger healthcare protection and better financial value. Thoughtful insurance planning supports continuous access to quality medical services while minimizing unnecessary expenses. Understanding plan differences empowers individuals and families to confidently choose healthcare coverage that supports long-term wellness and financial security.

Understanding Copayments Within PPO And HMO Insurance Plans

Copayments are an important cost factor when comparing PPO vs HMO health plans. These fixed payments apply to physician visits, specialist appointments, urgent care, prescription medications, and other covered healthcare services. HMO plans often feature lower copayments because they focus on coordinated in-network care, while PPO copayments may be higher due to greater provider flexibility. Understanding copayment structures allows consumers to estimate annual healthcare expenses more accurately while selecting insurance plans that balance affordability with comprehensive medical protection.

Managing Healthcare Costs Through Better Insurance Planning Strategies

Comparing PPO vs HMO health plans helps consumers create effective healthcare budgets while reducing unnecessary medical expenses. Evaluating premiums, deductibles, copayments, prescription costs, and annual out-of-pocket limits provides a complete financial picture before enrollment. Healthcare planning should consider expected doctor visits, specialist consultations, medications, and emergency care needs. Understanding total healthcare costs instead of monthly premiums alone helps consumers choose insurance that supports both medical requirements and long-term financial stability throughout the policy year.

Choosing Reliable Insurance Companies Offering Quality Healthcare Coverage

Selecting reputable insurers remains essential when comparing PPO vs HMO health plans. Consumers should review financial strength ratings, customer satisfaction, claims processing performance, provider network quality, and customer support before purchasing coverage. Reliable insurance companies consistently provide better healthcare experiences during medical treatment and claims resolution. Comparing insurer reputations alongside policy benefits helps consumers maximize long-term healthcare satisfaction while ensuring dependable financial protection against unexpected medical expenses and healthcare emergencies.

Preparing Medical Documents Before Filing Healthcare Insurance Claims

Maintaining organized medical records strengthens future claims under PPO vs HMO health plans. Consumers should keep insurance identification cards, physician reports, hospital discharge summaries, laboratory results, medical invoices, prescription receipts, and payment records safely organized. Proper documentation simplifies communication with healthcare providers and insurance companies while reducing administrative delays. Preparing records before emergencies occur improves claim accuracy and reimbursement speed. Organized healthcare documentation supports smoother insurance experiences while ensuring timely access to eligible medical benefits.

Reviewing Health Insurance Plans During Annual Enrollment Periods

Annual reviews of PPO vs HMO health plans help consumers identify stronger coverage, lower costs, expanded provider networks, and improved prescription benefits. Healthcare needs, financial circumstances, and preferred physicians often change over time. Insurance providers also update premiums and plan features annually. Comparing available options before renewing existing coverage ensures healthcare protection continues matching personal priorities. Regular insurance evaluations strengthen long-term financial planning while improving overall healthcare satisfaction and reducing unnecessary medical expenses.

Technology Transforming Modern PPO And HMO Healthcare Services

Technology continues improving PPO vs HMO health plans through telemedicine, mobile applications, digital insurance cards, electronic claims processing, secure customer portals, and artificial intelligence. Consumers can compare providers, monitor claims, schedule appointments, and manage policies conveniently through digital platforms. These innovations improve efficiency while reducing paperwork and administrative delays. Understanding available healthcare technology helps policyholders maximize insurance benefits while receiving faster support and improved healthcare experiences throughout their coverage period.

Future Innovations Shaping Healthcare Insurance Coverage Solutions

Healthcare continues evolving through artificial intelligence, wearable medical devices, predictive analytics, telemedicine expansion, and personalized treatment programs affecting PPO vs HMO health plans. Insurance companies increasingly adopt advanced technologies that improve healthcare accessibility, customer service, and claims efficiency. Consumers who understand future healthcare trends can better prepare for changing insurance markets and evolving medical services. Staying informed supports smarter healthcare planning while maximizing long-term insurance value and financial protection against future healthcare challenges.

Building Financial Security Through Comprehensive Health Insurance Coverage

Reliable PPO vs HMO health plans provide valuable financial protection against unexpected healthcare expenses resulting from illnesses, surgeries, hospitalizations, emergency treatment, and chronic medical conditions. Comprehensive health insurance helps preserve household savings while ensuring continued access to quality medical care. Consumers should view health insurance as an important component of long-term financial planning rather than simply a monthly expense. Strong healthcare coverage supports financial stability while providing lasting peace of mind for individuals and families.

Avoiding Common Healthcare Insurance Selection Mistakes Successfully Today

Many consumers comparing PPO vs HMO health plans choose coverage based solely on monthly premiums without considering provider flexibility, referral requirements, prescription benefits, deductibles, or anticipated healthcare needs. These mistakes may increase long-term medical expenses and reduce satisfaction with healthcare services. Comparing complete policy details instead of premiums alone results in smarter insurance decisions. Understanding common purchasing errors helps consumers maximize healthcare value while securing dependable long-term medical protection.

Choosing PPO Vs HMO Health Plans With Confidence Always

Selecting between PPO vs HMO health plans requires evaluating healthcare flexibility, provider networks, referral policies, specialist access, premiums, deductibles, prescription benefits, and expected medical usage. Consumers who carefully compare both options often obtain stronger healthcare protection while controlling long-term medical expenses. Well-informed insurance decisions improve healthcare accessibility, financial stability, and overall satisfaction. Regular policy reviews ensure healthcare coverage continues meeting changing personal and family needs while providing dependable protection throughout every stage of life.

Frequently Asked Questions

What is the main difference between PPO and HMO health plans?

PPO vs HMO health plans differ mainly in provider flexibility, referral requirements, and overall healthcare costs.

Which is better, PPO or HMO?

It depends on your healthcare needs. PPO offers greater flexibility, while HMO usually provides lower costs.

Do PPO plans require specialist referrals?

No. PPO plans generally allow direct access to specialists without referrals.

Can I see out-of-network doctors with an HMO?

Generally no, except for emergency medical situations.

Are PPO plans more expensive than HMO plans?

Yes, PPO plans usually have higher premiums and deductibles because they provide greater provider flexibility.

Which plan is best for families?

Families should compare healthcare needs, provider networks, specialist access, and overall annual healthcare costs before deciding.

Should frequent travelers choose PPO plans?

Yes. PPO plans usually offer broader provider access and better out-of-network coverage for travelers.

Conclusion

Choosing between PPO vs HMO health plans depends on your healthcare priorities, budget, and preferred level of provider flexibility. PPO plans offer greater freedom to choose doctors and specialists without referrals, making them ideal for individuals who value convenience and nationwide provider access. HMO plans, on the other hand, provide lower premiums and coordinated care that often reduces overall healthcare costs. Carefully comparing premiums, deductibles, provider networks, prescription benefits, and expected medical needs helps consumers select the most suitable health insurance plan. An informed decision today ensures better healthcare access, stronger financial protection, and long-term peace of mind for both individuals and families.