Introduction

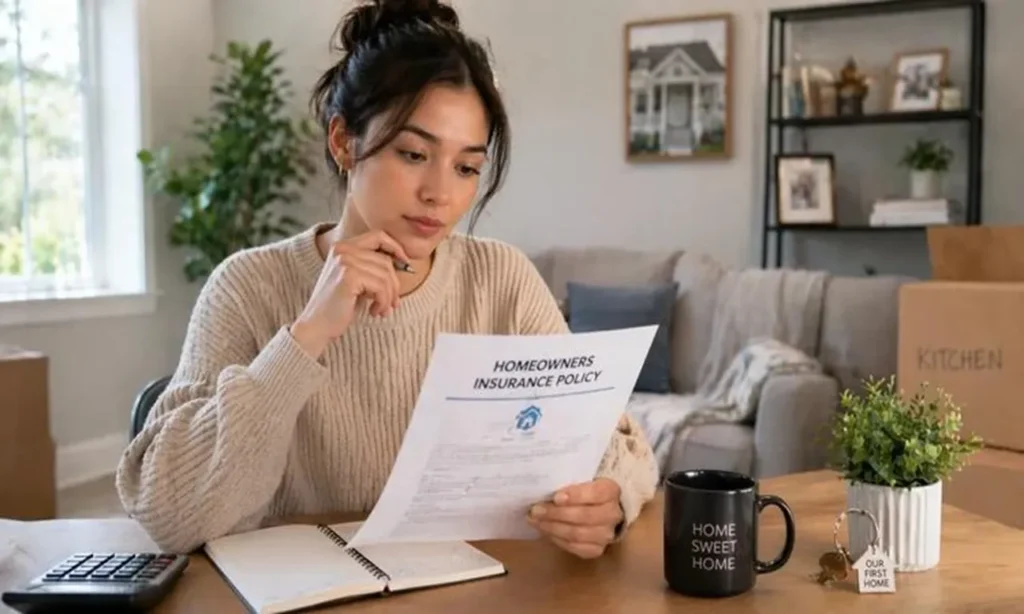

Home insurance claims process is an essential procedure every homeowner should understand before unexpected property damage occurs. Have you ever wondered what steps you should take immediately after a fire, storm, theft, or water damage affects your home? Many homeowners panic during emergencies and unknowingly make mistakes that delay or reduce claim settlements. Understanding the home insurance claims process helps you report losses correctly, gather the right evidence, cooperate with adjusters, and maximize your insurance benefits. Knowing what to expect before filing a claim reduces stress, speeds up recovery, and helps protect your financial investment while ensuring your insurance policy works exactly as intended.

Understanding Home Insurance Claims Process From Beginning Completely

The home insurance claims process begins immediately after a covered loss occurs. Whether the damage results from fire, storms, theft, or accidental water leaks, following the correct steps is essential for a successful claim. Homeowners should understand reporting requirements, documentation procedures, claim timelines, and insurer responsibilities before emergencies happen. Proper preparation reduces confusion and helps avoid unnecessary delays during recovery. Learning how the claims process works improves confidence while increasing the likelihood of receiving fair compensation for covered property damage and financial losses.

Reporting Property Damage Immediately After Covered Losses Occur

Promptly reporting damage is one of the most important steps in the home insurance claims process. Insurance companies generally require policyholders to notify them as soon as possible after discovering covered damage. Delayed reporting may complicate investigations or affect claim outcomes. Homeowners should provide accurate information regarding the incident while following insurer instructions carefully. Quick communication allows insurance companies to begin inspections and claim evaluations sooner. Timely reporting supports faster claim processing while helping homeowners begin repairs and financial recovery more efficiently.

Protecting Your Property From Additional Damage Immediately Afterwards

After a covered incident occurs, homeowners should take reasonable steps to prevent additional damage whenever it is safe to do so. The home insurance claims process often expects policyholders to protect their property from worsening conditions. Temporary repairs such as covering damaged roofs, shutting off leaking water, or boarding broken windows may reduce future losses. Keeping receipts for emergency repairs helps support reimbursement requests. Acting responsibly strengthens claim credibility while demonstrating efforts to minimize damages before permanent restoration begins.

Documenting Damage Thoroughly Before Starting Any Repairs Carefully

Accurate documentation is critical for a successful home insurance claims process. Homeowners should photograph and video every damaged area before removing debris or beginning repairs whenever possible. Detailed images provide valuable evidence supporting claim evaluations and settlement negotiations. Written inventories describing damaged belongings, estimated values, and purchase information further strengthen documentation. Maintaining organized records improves communication with insurance adjusters. Comprehensive evidence helps prevent disputes while increasing the likelihood of receiving fair compensation for covered property losses and repair expenses.

Creating Detailed Inventory Of Damaged Personal Property Items

Preparing a complete inventory of damaged belongings is an essential part of the home insurance claims process. Homeowners should list furniture, electronics, appliances, clothing, jewelry, and other affected possessions along with estimated replacement values. Receipts, serial numbers, photographs, and warranty documents further strengthen claim documentation. Organized inventories simplify insurer evaluations while reducing disagreements regarding ownership or value. Accurate records improve claim efficiency and help homeowners recover financial losses more effectively following covered property damage and unexpected household disasters.

Understanding Your Insurance Policy Before Filing Claims Successfully

Every homeowner should review policy terms before beginning the home insurance claims process. Understanding coverage limits, deductibles, exclusions, endorsements, and reporting requirements prevents confusion during stressful situations. Many claim disputes result from misunderstandings regarding policy benefits rather than insurer mistakes. Reading policy documents carefully allows homeowners to understand what damages qualify for coverage and which expenses remain their responsibility. Better policy knowledge strengthens claim preparation while improving communication with insurance representatives throughout the entire settlement process.

Working With Insurance Adjusters During Property Inspections Professionally

Insurance adjusters play a central role in the home insurance claims process by evaluating property damage and estimating repair costs. Homeowners should accompany adjusters during inspections whenever possible to answer questions and highlight all damaged areas. Honest communication and complete documentation improve inspection accuracy. Keeping personal notes regarding inspection discussions provides useful references later. Positive cooperation helps streamline claim evaluations while ensuring adjusters receive complete information needed to prepare accurate damage assessments and fair settlement recommendations.

Understanding Deductibles Affecting Final Insurance Claim Payments Clearly

Deductibles represent the portion of covered losses homeowners pay before insurance benefits apply. During the home insurance claims process, understanding deductible amounts helps policyholders estimate expected claim payments more accurately. Higher deductibles generally reduce annual premiums but increase personal expenses after losses occur. Reviewing deductible responsibilities before filing claims prevents misunderstandings regarding final settlement amounts. Knowing how deductibles influence payments supports better financial planning while preparing homeowners for repair expenses following covered property damage.

Obtaining Repair Estimates From Qualified Licensed Contractors Properly

Independent repair estimates provide valuable support throughout the home insurance claims process. Homeowners should obtain written estimates from reputable, licensed contractors experienced with similar property damage. Multiple estimates improve pricing accuracy while helping homeowners compare recommended repairs. Detailed proposals strengthen negotiations if settlement amounts appear insufficient. Choosing qualified professionals also reduces future repair complications. Reliable contractor estimates support fair insurance settlements while ensuring restoration work meets local construction standards and long-term quality expectations.

Temporary Living Expenses Covered During Major Home Repairs

When covered damage makes a home temporarily uninhabitable, many policies provide additional living expense benefits through the home insurance claims process. These benefits may help pay for hotel accommodations, meals, transportation, and temporary housing during repairs. Understanding available assistance helps homeowners prepare financially before disasters occur. Keeping receipts for eligible expenses strengthens reimbursement requests. Proper documentation supports smoother claim processing while helping families maintain comfortable living arrangements throughout lengthy property restoration and rebuilding projects.

Avoiding Common Mistakes During Insurance Claims Filing Process

Many homeowners unintentionally delay the home insurance claims process by making preventable mistakes. Waiting too long to report damage, failing to document losses, discarding damaged property too quickly, providing incomplete information, or beginning repairs without approval can complicate claims. Understanding these common errors helps homeowners avoid unnecessary problems during settlement negotiations. Careful preparation strengthens claim credibility while improving communication with insurers. Avoiding simple mistakes increases the likelihood of faster approvals and fair financial compensation following covered property losses.

Maintaining Organized Records Throughout Entire Claims Process Successfully

Well-organized records significantly improve the home insurance claims process from beginning to final settlement. Homeowners should maintain copies of claim forms, repair estimates, photographs, receipts, correspondence, inspection reports, and payment records. Organized documentation simplifies communication with insurers while providing valuable evidence if disputes arise. Keeping chronological records improves claim management and reduces unnecessary confusion. Strong recordkeeping practices help homeowners monitor progress while supporting efficient claim resolution and accurate reimbursement for covered property damage.

Communicating Clearly With Insurance Representatives During Every Step

Clear and professional communication strengthens every stage of the home insurance claims process. Homeowners should respond promptly to requests for information while asking questions whenever policy terms or settlement decisions appear unclear. Maintaining written records of conversations, emails, and claim updates improves accountability throughout the process. Respectful communication encourages productive working relationships with insurance representatives. Consistent cooperation helps reduce misunderstandings while supporting faster claim evaluations, smoother negotiations, and successful property restoration after covered losses.

Knowing Your Rights During Insurance Claim Settlements Properly

Understanding policyholder rights is an important part of the home insurance claims process. Homeowners have the right to receive timely claim evaluations, fair settlement explanations, and clear communication regarding coverage decisions. If disagreements occur, policyholders may request additional reviews, submit supporting evidence, or seek professional assistance. Understanding these rights improves confidence throughout claim negotiations. Informed homeowners communicate more effectively while protecting their financial interests during complex insurance settlement discussions following covered property damage.

Preparing Financially Before Unexpected Home Insurance Claims Happen

Preparation before disasters occur makes the home insurance claims process much easier to manage. Maintaining emergency savings, updated home inventories, digital copies of insurance documents, contractor contacts, and emergency response plans improves overall readiness. Understanding insurance responsibilities before filing claims reduces stress during unexpected situations. Proactive planning strengthens financial resilience while allowing homeowners to respond quickly after covered losses. Careful preparation supports smoother claims, faster recoveries, and greater confidence when protecting valuable residential property investments.

Understanding Policy Exclusions Before Filing Insurance Claims Carefully

Every insurance policy contains exclusions that affect the home insurance claims process. Certain losses such as floods, earthquakes, neglect, intentional damage, and normal wear and tear may not qualify for reimbursement under standard policies. Understanding these exclusions before filing a claim helps homeowners avoid disappointment and unnecessary disputes. Reviewing policy documents carefully improves awareness of covered and uncovered situations. Better knowledge of exclusions supports informed claim decisions while helping homeowners pursue compensation only for eligible property damage covered under their insurance agreement.

Flood Damage Requires Separate Insurance Claims Procedures Usually

Standard homeowners insurance generally excludes flood damage, requiring separate flood insurance for covered losses. During the home insurance claims process, understanding the difference between water damage and flooding helps homeowners file claims correctly. Burst pipes may qualify under homeowners insurance, while rising floodwater typically requires separate flood coverage. Reviewing policy terms before emergencies occur prevents misunderstandings later. Knowing which insurer handles specific losses improves claim efficiency while helping homeowners receive appropriate compensation through the correct insurance policy.

Replacement Cost Coverage Increases Insurance Settlement Amounts Significantly

Replacement cost protection plays an important role throughout the home insurance claims process by allowing homeowners to rebuild or replace damaged property using current market costs instead of depreciated values. This coverage generally provides higher settlements than actual cash value policies after covered losses occur. Understanding replacement cost benefits helps homeowners evaluate insurance policies before disasters happen. Strong replacement cost coverage reduces financial burdens while supporting faster recovery, accurate rebuilding, and improved long-term financial security following significant property damage.

Actual Cash Value Claims Explained For Homeowners Clearly Today

Actual cash value coverage calculates insurance settlements by subtracting depreciation from replacement costs during the home insurance claims process. Although these policies often carry lower premiums, they may result in smaller claim payments following covered losses. Understanding depreciation helps homeowners estimate settlement expectations more accurately before filing claims. Reviewing valuation methods carefully strengthens insurance planning while reducing future surprises. Selecting appropriate coverage supports balanced financial decisions and helps homeowners prepare for potential out-of-pocket rebuilding or replacement expenses after disasters.

Independent Public Adjusters Assisting Complex Insurance Claims Successfully

Some homeowners choose independent public adjusters to assist with complicated home insurance claims process situations involving extensive damage or disputed settlements. Public adjusters work on behalf of policyholders by reviewing damages, documenting losses, and negotiating claim settlements with insurance companies. Understanding when professional assistance becomes beneficial helps homeowners protect financial interests more effectively. Experienced adjusters often improve documentation quality while strengthening claim presentations. Professional guidance supports fair negotiations and helps policyholders navigate complex insurance procedures following significant covered property damage.

How Previous Claims Influence Future Insurance Premium Costs

Insurance companies often evaluate previous claims when calculating future premiums after completing the home insurance claims process. Multiple claims within short periods may increase insurance costs or affect eligibility for preferred pricing. Understanding how claim history influences underwriting decisions helps homeowners evaluate whether smaller losses should be reported. Preventive maintenance and responsible property care reduce unnecessary claims over time. Maintaining favorable insurance records contributes to long-term affordability while supporting stronger relationships with insurance providers and improved policy options.

Financial Strength Matters When Selecting Insurance Companies Wisely

Choosing a financially stable insurance company improves confidence throughout the home insurance claims process. Strong insurers possess sufficient financial resources to process and pay claims efficiently, even after widespread disasters affecting many policyholders simultaneously. Independent rating agencies evaluate insurer financial performance and long-term reliability. Understanding financial ratings helps homeowners compare companies beyond premium prices alone. Selecting financially secure providers strengthens long-term protection while ensuring dependable financial support remains available whenever covered property losses require prompt claim assistance.

Customer Service Quality Improves Entire Claims Experience Significantly

Excellent customer service greatly influences satisfaction throughout the home insurance claims process. Homeowners benefit from responsive communication, knowledgeable representatives, efficient claim handling, and timely updates regarding settlement progress. Understanding customer service quality helps consumers evaluate insurance providers before purchasing policies. Customer reviews and satisfaction ratings offer valuable insights into insurer performance. Reliable service reduces stress while supporting smoother claim experiences, stronger communication, and faster recovery after covered property damage affects residential homes.

Digital Claims Technology Speeds Insurance Processing Efficiently Today

Modern technology has transformed the home insurance claims process through online claim reporting, mobile applications, digital document uploads, electronic signatures, and virtual property inspections. These innovations simplify claim administration while improving communication between homeowners and insurers. Understanding available digital tools helps policyholders manage claims more efficiently before and after property losses occur. Faster technology reduces paperwork while improving transparency. Digital claims platforms strengthen customer experiences and support quicker insurance settlements following covered disasters.

Annual Policy Reviews Prevent Future Insurance Claim Problems

Regular insurance reviews strengthen the home insurance claims process by ensuring coverage remains accurate before disasters occur. Property improvements, inflation, valuable purchases, and family changes may require policy updates over time. Reviewing insurance annually helps homeowners avoid underinsurance and coverage gaps that complicate future claims. Updated policies improve financial protection while reflecting current rebuilding costs and personal property values. Consistent reviews strengthen preparedness and support smoother insurance settlements whenever covered property losses arise unexpectedly.

Inflation Impacts Future Home Insurance Claim Settlement Values

Inflation steadily increases construction costs, labor expenses, and replacement values that influence the home insurance claims process. Coverage limits that once appeared adequate may become insufficient after several years. Understanding inflation encourages homeowners to review policy limits regularly and maintain appropriate financial protection. Many insurers provide inflation guard features that automatically increase coverage amounts. Keeping policies current reduces unexpected rebuilding expenses while supporting stronger claim settlements after significant covered property damage requiring extensive repairs or reconstruction.

Emergency Preparedness Supports Faster Insurance Claim Recovery Together

Emergency preparedness complements the home insurance claims process by helping homeowners respond efficiently after disasters occur. Maintaining emergency kits, protecting insurance documents, preparing property inventories, and establishing evacuation plans improve readiness before unexpected events happen. Organized preparation simplifies claim documentation while reducing confusion during stressful situations. Insurance provides financial recovery, while preparedness accelerates restoration efforts. Combining comprehensive insurance with proactive emergency planning strengthens resilience and supports successful recovery after covered residential property losses.

Working With Contractors During Insurance Repair Projects Successfully

Qualified contractors play an important role throughout the home insurance claims process by preparing repair estimates, completing restoration work, and communicating with insurance adjusters when necessary. Homeowners should select licensed, insured, and reputable contractors experienced with insurance restoration projects. Comparing multiple estimates improves pricing accuracy while reducing future repair concerns. Strong contractor relationships support quality workmanship and timely project completion. Reliable professionals help homeowners restore damaged property efficiently following approved insurance settlements.

Understanding Insurance Claim Appeals After Settlement Disagreements Arise

Occasionally homeowners disagree with insurance settlement decisions during the home insurance claims process. Most insurers provide formal appeal procedures allowing policyholders to submit additional documentation, request reconsideration, or obtain independent evaluations. Understanding available appeal options helps homeowners protect financial interests when disagreements occur. Organized records and professional communication strengthen appeal requests significantly. Knowing policyholder rights encourages fair negotiations while improving opportunities to achieve reasonable claim resolutions after covered property damage.

Building Long-Term Financial Security Through Smart Insurance Planning

Successful financial planning includes understanding the home insurance claims process long before disasters occur. Maintaining accurate coverage, updating inventories, reviewing policies annually, and preparing emergency documentation all strengthen future claim outcomes. Proactive insurance management reduces financial uncertainty while improving recovery following unexpected property losses. Thoughtful planning helps homeowners preserve valuable assets and maintain confidence during difficult situations. Strong insurance preparation supports long-term financial security while ensuring claims proceed as smoothly and efficiently as possible whenever covered events occur.

Avoiding Common Home Insurance Claim Filing Mistakes Completely

Many homeowners unintentionally complicate the home insurance claims process by making preventable mistakes immediately after property damage occurs. Delaying claim reporting, discarding damaged items too early, failing to document losses, or beginning repairs without insurer approval can reduce settlement amounts. Understanding these common errors helps policyholders protect their financial interests. Careful documentation, prompt communication, and organized records strengthen claim credibility while improving settlement outcomes. Avoiding simple mistakes helps homeowners achieve faster approvals and smoother financial recovery following covered property losses.

Understanding Home Insurance Claim Settlement Payment Options Available

Insurance companies may issue claim payments in several ways depending on policy terms and damage severity. During the home insurance claims process, payments may be made directly to homeowners, contractors, or mortgage lenders when applicable. Some settlements are released in multiple stages as repairs progress. Understanding payment methods helps homeowners manage rebuilding expenses more effectively. Reviewing settlement procedures reduces confusion while improving financial planning. Knowledge of payment options supports smoother restoration projects and better overall claim experiences after covered losses.

Protecting Valuable Property During Insurance Claim Investigations Properly

Homeowners should preserve damaged property whenever possible until insurance inspections are completed. Throughout the home insurance claims process, damaged items often serve as important evidence supporting claim evaluations. Removing debris too quickly or disposing of damaged belongings without approval may complicate investigations. Photographing every affected area and keeping damaged items available for inspection strengthens documentation. Proper evidence preservation improves claim accuracy while increasing the likelihood of receiving fair compensation for covered property damage and personal belongings.

Mortgage Companies During Home Insurance Claim Settlement Process

If a home carries an active mortgage, lenders may become involved during the home insurance claims process because they have a financial interest in the property. Insurance settlement checks are often issued jointly to homeowners and mortgage companies for significant structural repairs. Understanding lender involvement helps homeowners prepare for additional paperwork and payment procedures. Maintaining communication with both parties improves claim efficiency. Awareness of mortgage requirements supports smoother restoration projects while preventing unnecessary delays in receiving repair funds.

Working Successfully With Restoration Companies After Property Damage

Professional restoration companies frequently assist homeowners during the home insurance claims process by providing emergency cleanup, water extraction, smoke removal, mold prevention, and structural drying services. Choosing experienced, licensed restoration professionals improves repair quality and minimizes additional property damage. Understanding restoration procedures helps homeowners coordinate effectively with insurers and contractors. Prompt professional assistance strengthens recovery efforts while reducing future repair expenses. Reliable restoration services support successful claim outcomes and faster return to normal living conditions.

Managing Temporary Repair Expenses Before Insurance Reimbursement Arrives

Emergency repairs often become necessary before final insurance settlements are completed. During the home insurance claims process, homeowners may need to cover temporary expenses such as roof tarps, boarded windows, plumbing repairs, or water removal services. Keeping detailed receipts and invoices supports reimbursement requests later. Understanding temporary repair responsibilities prevents further property damage while strengthening insurance claims. Proper documentation ensures homeowners recover eligible emergency expenses and maintain property safety throughout the restoration process.

Maintaining Accurate Communication Records Throughout Entire Claim Process

Detailed communication records play an important role in the home insurance claims process. Homeowners should maintain written notes regarding phone conversations, emails, claim updates, inspection dates, payment discussions, and adjuster recommendations. Organized records improve accountability while helping resolve misunderstandings efficiently. Documentation provides valuable evidence if disagreements arise regarding settlement decisions or claim timelines. Strong communication practices strengthen negotiations while supporting smoother claim management from initial reporting through final property restoration and financial reimbursement.

How Independent Inspections Strengthen Insurance Claim Negotiations Better

Independent property inspections can provide valuable support during complicated home insurance claims process situations. Qualified inspectors or engineers may identify hidden structural damage overlooked during initial evaluations. Independent reports strengthen negotiations by providing objective evidence supporting additional repair requirements. Homeowners benefit from comprehensive assessments that accurately reflect actual property conditions. Professional inspections improve claim documentation while increasing opportunities for fair settlements when significant property damage affects structural integrity and long-term safety.

Choosing Qualified Contractors After Insurance Claim Approval Carefully

Selecting experienced contractors remains essential after insurance claim approval. Throughout the home insurance claims process, homeowners should verify contractor licensing, insurance, references, warranties, and project timelines before signing agreements. Comparing multiple proposals improves pricing transparency and construction quality. Reliable contractors communicate effectively with insurance companies while completing repairs according to industry standards. Careful contractor selection strengthens restoration outcomes while protecting homeowners from unnecessary delays, poor workmanship, and additional financial complications after covered property damage.

Understanding Supplemental Claims For Hidden Property Damage Later

Additional hidden damage sometimes appears after repair work begins. The home insurance claims process often allows supplemental claims when previously undiscovered covered damage is identified during restoration. Contractors frequently uncover structural issues, water intrusion, electrical problems, or foundation damage requiring additional repairs. Understanding supplemental claim procedures helps homeowners secure appropriate reimbursement for newly discovered covered losses. Prompt reporting and detailed documentation strengthen supplemental requests while supporting complete property restoration and financial recovery.

Technology Improving Home Insurance Claim Management Every Year

Modern technology continues transforming the home insurance claims process through artificial intelligence, drone inspections, mobile claim applications, virtual property assessments, and automated document management. These innovations improve efficiency while reducing claim processing times and communication delays. Understanding technological advancements helps homeowners take advantage of faster reporting and digital claim tracking. Modern insurance platforms strengthen transparency while simplifying policy management. Technology enhances customer experiences and supports quicker settlements following covered residential property losses.

Environmental Risks Increasing Future Insurance Claim Complexity Today

Changing environmental conditions continue influencing the home insurance claims process by increasing the frequency and severity of storms, wildfires, hail, and severe weather events. Larger disasters often generate more complex insurance claims requiring extensive documentation and inspections. Understanding evolving environmental risks encourages homeowners to maintain adequate insurance coverage and emergency preparedness. Regular policy reviews strengthen financial protection while supporting smoother recovery after increasingly severe natural disasters affecting residential properties.

Choosing Trusted Insurance Providers For Reliable Claim Support

Reliable insurance providers play a major role in successful home insurance claims process experiences. Homeowners should evaluate insurer financial strength, customer satisfaction, claims handling performance, digital capabilities, and industry reputation before purchasing coverage. Understanding provider reliability helps consumers select companies capable of delivering dependable assistance during emergencies. Strong insurers consistently provide efficient communication and fair claim handling. Choosing trusted insurance companies strengthens long-term confidence while ensuring reliable financial support following covered property losses.

Building Long-Term Confidence Through Insurance Claims Knowledge Together

Understanding the home insurance claims process before disasters occur gives homeowners greater confidence during stressful situations. Regular policy reviews, organized documentation, emergency preparedness, and strong communication skills all contribute to successful claim outcomes. Learning how claims work reduces uncertainty while improving financial recovery following covered losses. Proactive insurance management strengthens long-term resilience and protects valuable property investments. Well-informed homeowners navigate claims more efficiently while preserving financial stability and minimizing disruption after unexpected residential property damage.

Final Thoughts About Home Insurance Claims Process Success

The home insurance claims process becomes far less stressful when homeowners understand each step before emergencies occur. Prompt reporting, accurate documentation, organized records, professional communication, and careful policy reviews all contribute to successful claim outcomes. Working closely with adjusters, contractors, and insurance representatives helps ensure repairs proceed efficiently and settlements remain fair. Maintaining updated insurance coverage and preparing before disasters happen further strengthens financial protection. By learning the complete claims process in advance, homeowners can recover more quickly, reduce unnecessary delays, protect valuable property investments, and confidently navigate future insurance claims with greater peace of mind.

FAQs

What is the home insurance claims process?

The home insurance claims process is the procedure homeowners follow to report damage, document losses, work with adjusters, and receive compensation for covered events.

How soon should I report a home insurance claim?

You should report a covered loss as soon as possible to help avoid delays and support a faster claim investigation.

What documents are needed for a home insurance claim?

Photographs, videos, receipts, repair estimates, home inventories, police reports when applicable, and insurance policy details are commonly required.

Can I start repairs before the insurance adjuster arrives?

You may perform temporary emergency repairs to prevent further damage, but major repairs should generally wait until the insurer authorizes them.

How long does the home insurance claims process take?

The timeline depends on the severity of the damage, documentation, inspections, and the insurance company’s claim procedures.

What should I do if my insurance claim is denied?

Review the denial letter, provide additional supporting evidence, request reconsideration, or file a formal appeal according to your policy.

Does filing a home insurance claim increase premiums?

It can. Multiple claims or significant losses may affect future premiums depending on your insurer and claim history.

Conclusion

The home insurance claims process plays a crucial role in helping homeowners recover financially after unexpected property damage. Understanding every stage—from reporting the loss and documenting evidence to working with adjusters and completing repairs—helps minimize delays and improves settlement outcomes. Careful recordkeeping, prompt communication, and knowledge of your policy strengthen your position throughout the claims journey. Regular policy reviews and emergency preparedness further reduce financial uncertainty before disasters occur. By learning how the claims process works before you need it, homeowners can navigate stressful situations with greater confidence, protect valuable investments, and achieve faster, fairer claim resolutions while maintaining long-term financial security.